Blockchain is an exciting new technology that is already completely changing the world.

It’s the foundational driving force behind tons of exciting new technologies. The most famous example is, of course, Bitcoin – but these days, blockchain can be found in all sorts of different tools, applications and services.

Examples include securely sharing medical data, tracking music royalties for artists, cross-border payments, identity theft prevention, and much more.

While opinions vary on how important Bitcoin will be to the economy of the future, experts agree that blockchain is here to stay. So today, we’re taking a closer look at this nascent technology on the rise. We’ll answer: What is blockchain? Why is “removing trust” actually a good thing? What does it have to do with Bitcoin?

Let’s dive in!

First things first: What is blockchain, exactly?

Simply put, blockchain is “a distributed, decentralized, public ledger that eliminates the need for trust in transactions”.

Okay… so maybe that’s not exactly simple. Unless you work in finance or crypto-technology, you may not immediately understand the importance of a “decentralized public ledger”. So let’s break it down!

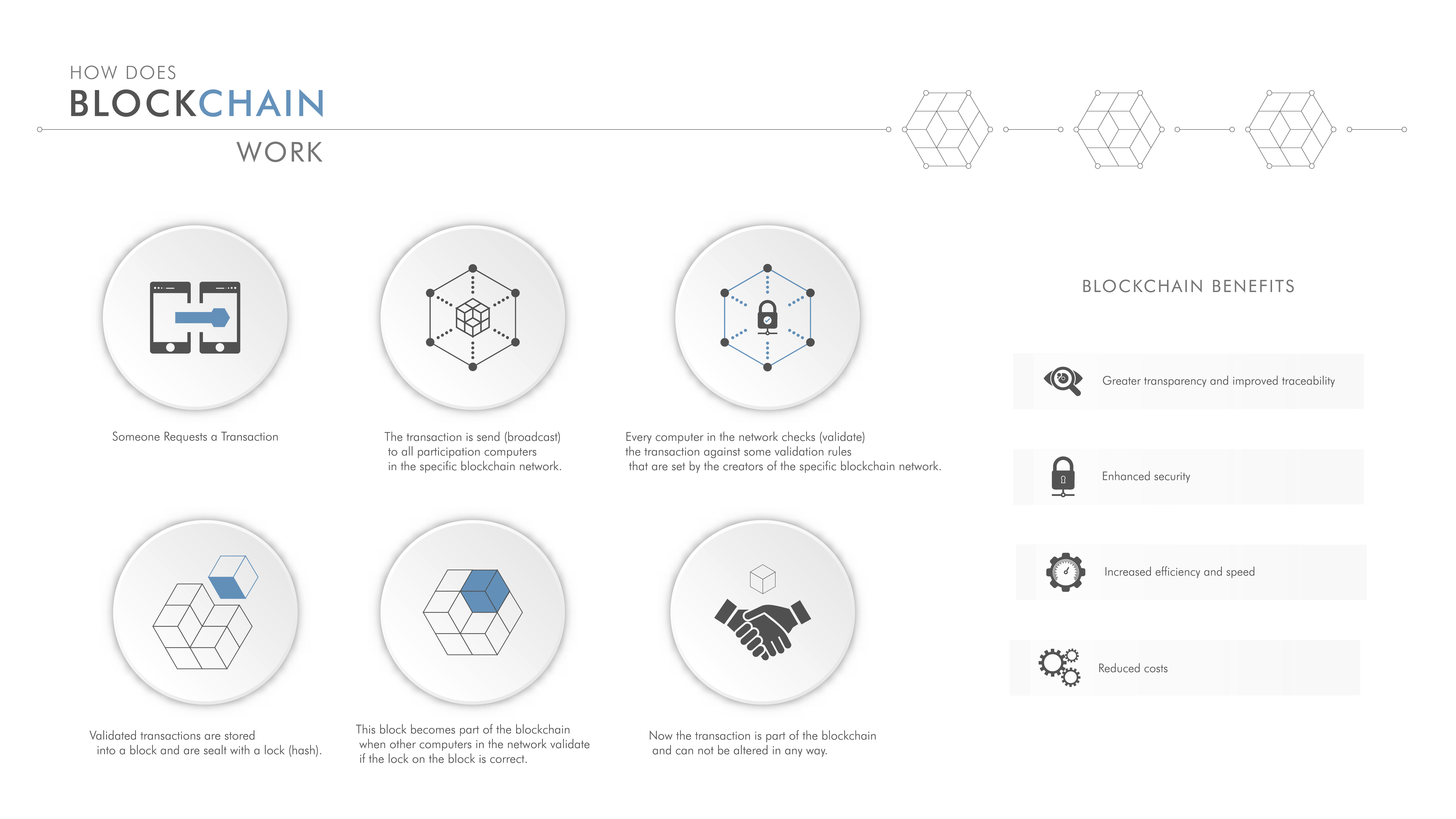

First off, the “blocks” refer to pieces of information, and the “chain” is like a record of all the blocks of information that have been processed so far.

Each “block” in the blockchain represents a specific piece of information. Usually it’s a transaction amount, or a date, or a verification code – but it can really be any piece of information.

Over time, these blocks are recorded by a series of independent computers – creating the “blockchain”.

That means you can think of blockchain as a “shared record of transactions”.

Uhh… maybe an example will help.

Let’s use transactions at the bank as our example. When you come in and deposit money, the bank records that deposit to your account. This is done by a human (who is prone to errors) and recorded in the bank’s own private system.

Now, let’s say you go to the bank one day, and they tell you that your account is empty – even though you know it’s not.

It’s your word against theirs, right?

Blockchain eliminates this possibility by “decentralizing” the ledger (AKA record of transactions).

With blockchain, the bank isn’t the only one recording the transactions. Imagine if, every time you made a deposit to your account, you also had 10 other independent witnesses verify the deposit.

Your bank couldn’t claim that your account was empty… because those 10 other witnesses would speak up, showing proof of your deposit.

This results in a “trustless transaction” – where no single party needs to be trusted, yet the result is trustworthy.

That’s basically how blockchain works. Instead of one entity controlling all the transactions, it involves multiple, independent, unbiased entities. This means there’s no longer a need for trust – instead, everything can be proven by a network of independent “observers” of the transaction.

Now, don’t get us wrong here – it’s unlikely your bank would pull something like this. It’s fair to say that you can certainly trust your bank. This was just an example. But since this technology exists now, the question finance and tech experts are asking is: “why not eliminate the need for trust?”

And of course, banks aren’t even the main focus of blockchain. This fundamental technology can be used in all sorts of situations, from retail purchases to managing currency to transferring medical records safely and more.

Any time the passing of information needs to be securely recorded, blockchain can step in and provide the proof needed to ensure everything is done fairly.

This “replacement for trust” is the basis behind Cryptocurrencies like Bitcoin.

Until recently, computers weren’t common or powerful enough to support such a “chain” of independent record-keepers.

But now they are… and that’s why Bitcoin and other cryptocurrencies have become so popular. They’re the ultimate example of blockchain: An entire currency that’s independently managed by everyone who owns it.

Unlike any currency issued privately by a central government, cryptocurrencies rely on blockchain to create a public currency that nobody controls.

That’s why some tech and finance experts are so excited about it. Instead of having to trust a government – which, let’s be honest, can make mistakes (or worse) – cryptocurrencies rely on giant webs of computers to oversee the transactions.

In the world of blockchain and cryptocurrency, nobody is in charge. Everything can be trusted, because no single entity has to be trusted. Everything is recorded in the blockchain, then heavily encrypted to prevent tampering.

Alright – now you know more about blockchain than most people ever will!

This is the most simple explanation of blockchain we could come up with. It’s a new technology with tons of exciting applications, and we expect it to become more popular over time – including the cryptocurrencies that it makes possible.

Of course, cryptocurrencies are a whole can of worms in their own right… and we’ll explain how they work in another episode of Innovations Explained. But this is plenty to wrap your head around for one day, right?

Alright, that’s all we’ve got for you (for now). What do you think about blockchain? Is it the future of information management, or is it just a fascinating fad that will pass? Let us know in the comments below – and if you have any questions about blockchain, drop those there too!

I wouldn’t trust it I don’t think tell me about people messing with things just never ever works out

Blockchain? How is it secure???